Intro

- Price floor discovered. 2015 price levels were too low to incentivize mining capex and recycling. Jewelry buyers and physical investors jumped into the market when prices fell below $1,100.

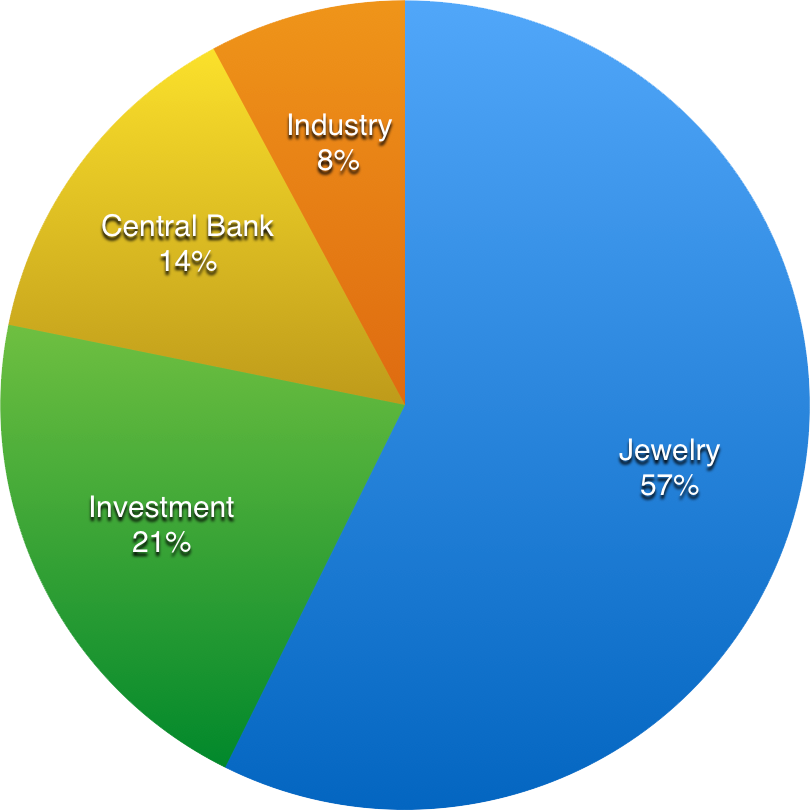

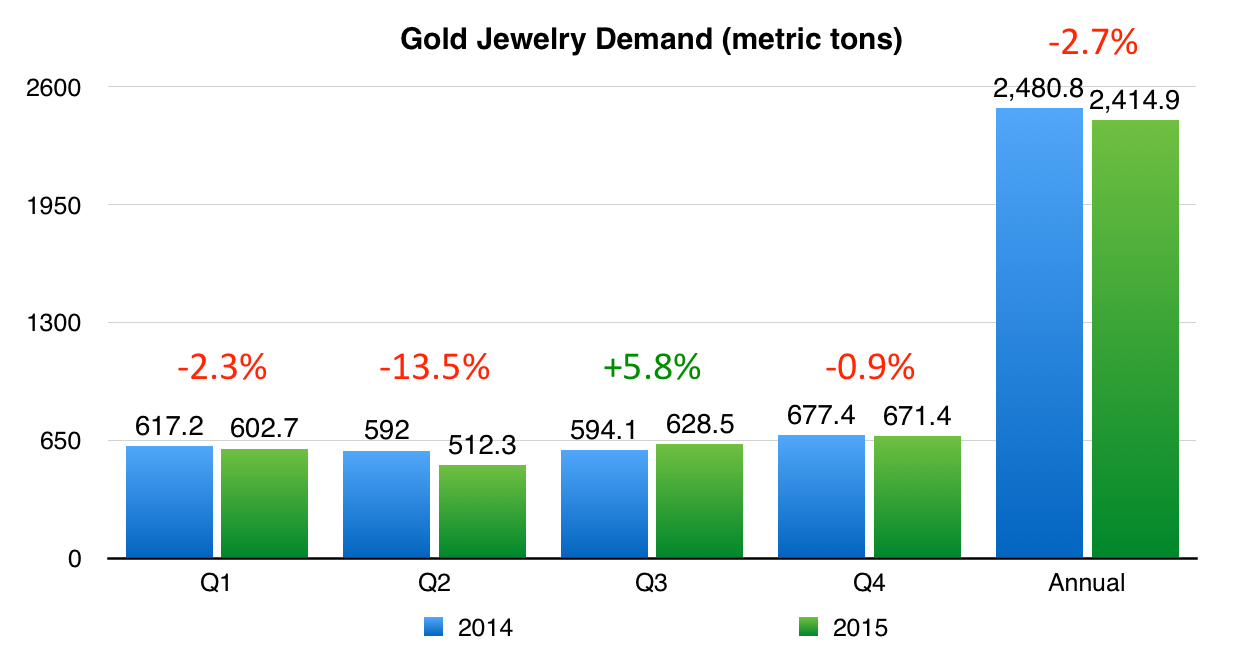

- Chinese demand increases as economic uncertainty, yuan devaluation, and capital controls persist.

- Indian demand dampened by transitory effects, but jewelry demand was still strong. Overall demand should rebound if weather is more favorable.

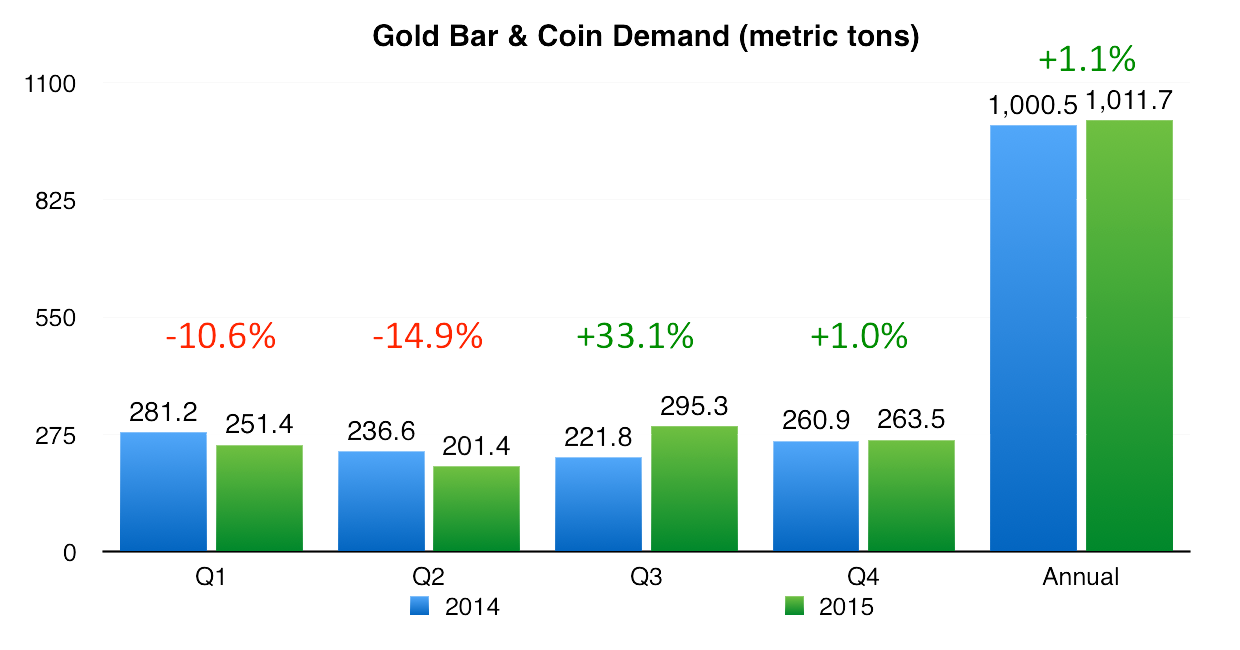

- Germany has become a stronger buyer of bars and coins to help offset falling demand from traditional sources: Turkey, Russia, and the Middle East.

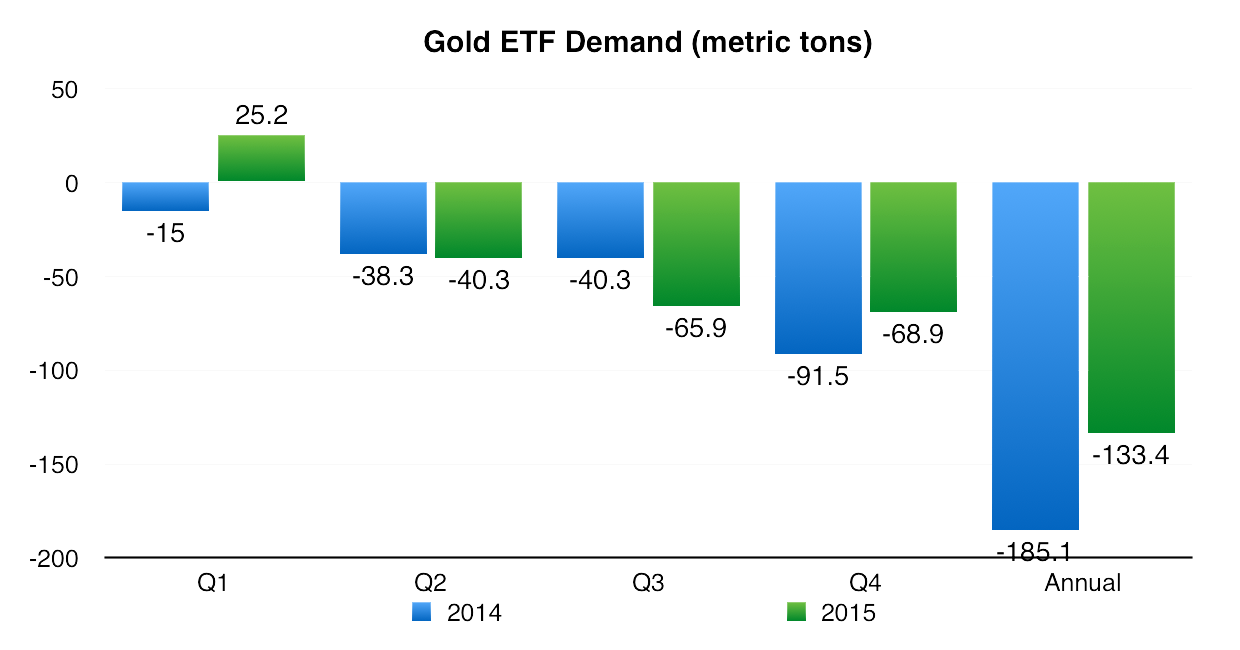

- ETFs have been sellers of gold for years. The return of gold ETF buying would significantly change the gold supply and demand balance.

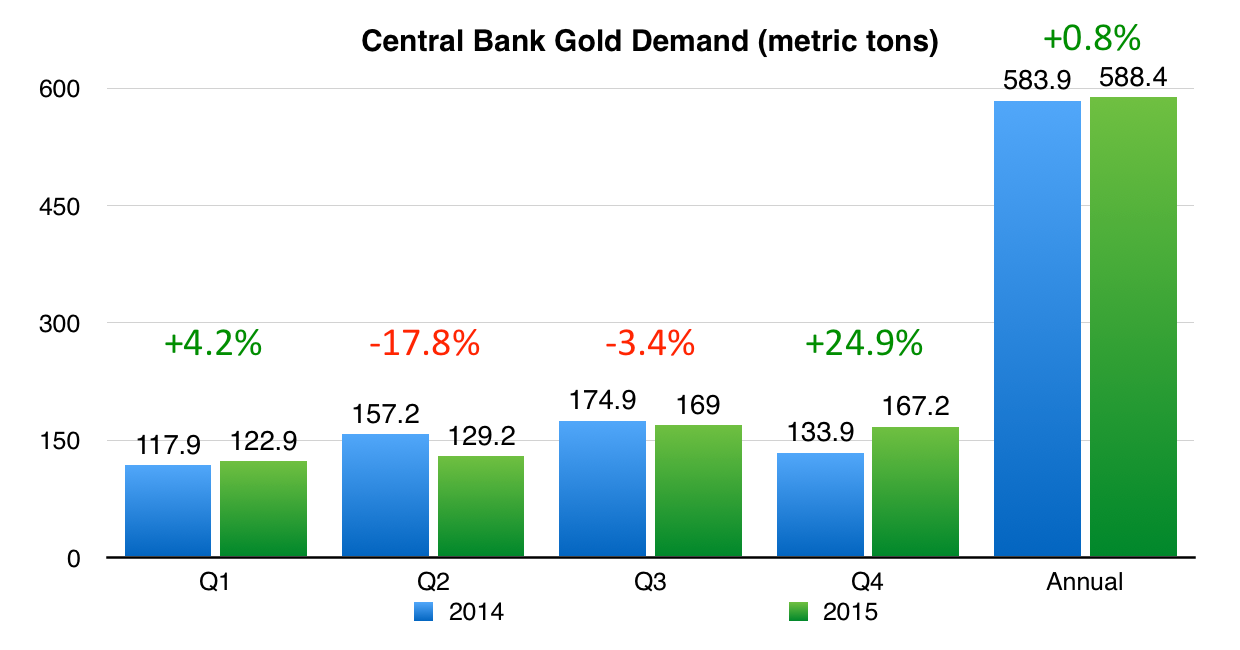

- Central banks continue to be a firm source of demand.

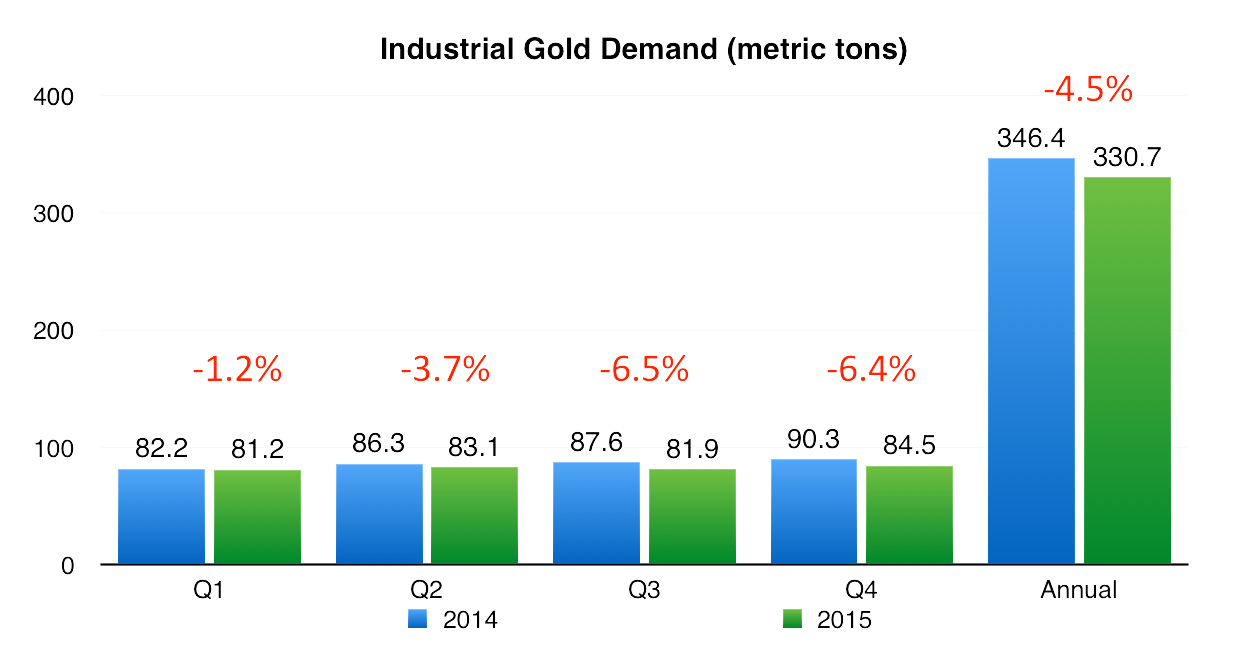

- Industrial demand continues to decline but is a relatively small drag on demand.

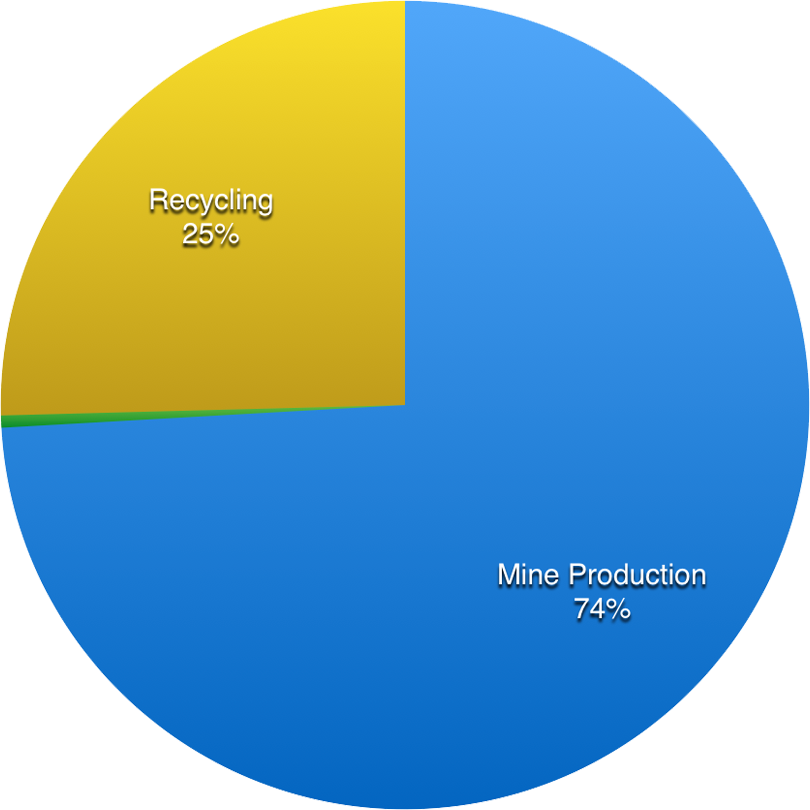

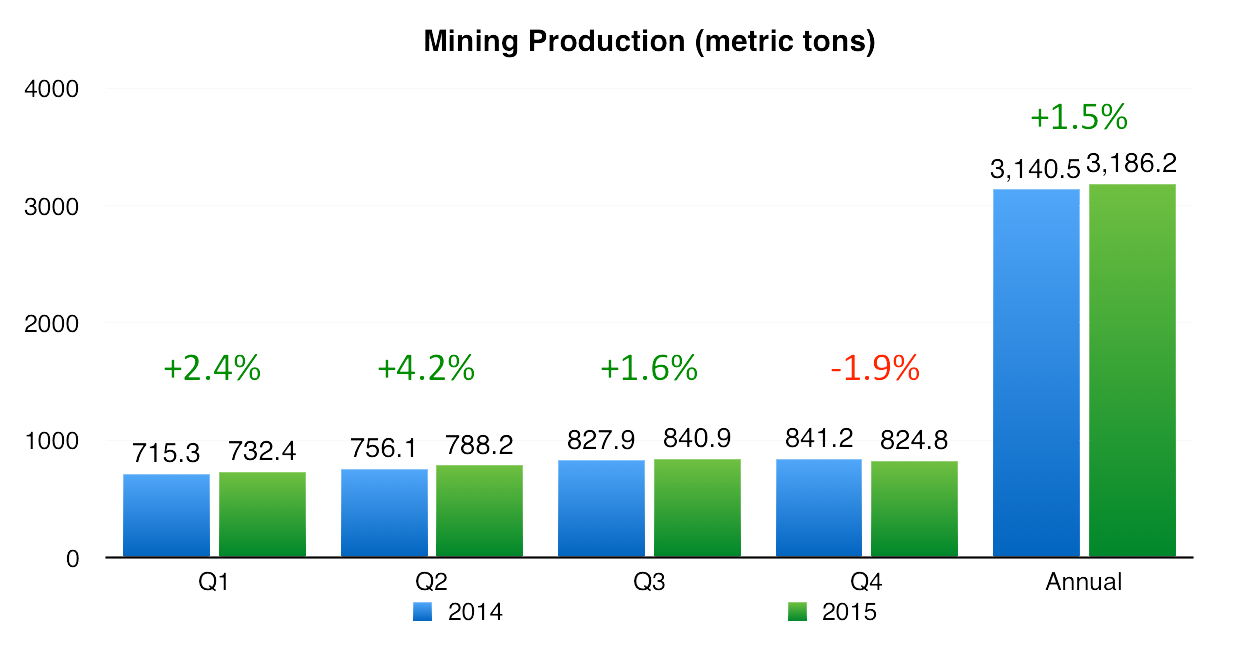

- Mining production declines are the result of cost cuts, aging mines, lower grade veins, and years of declining capex.

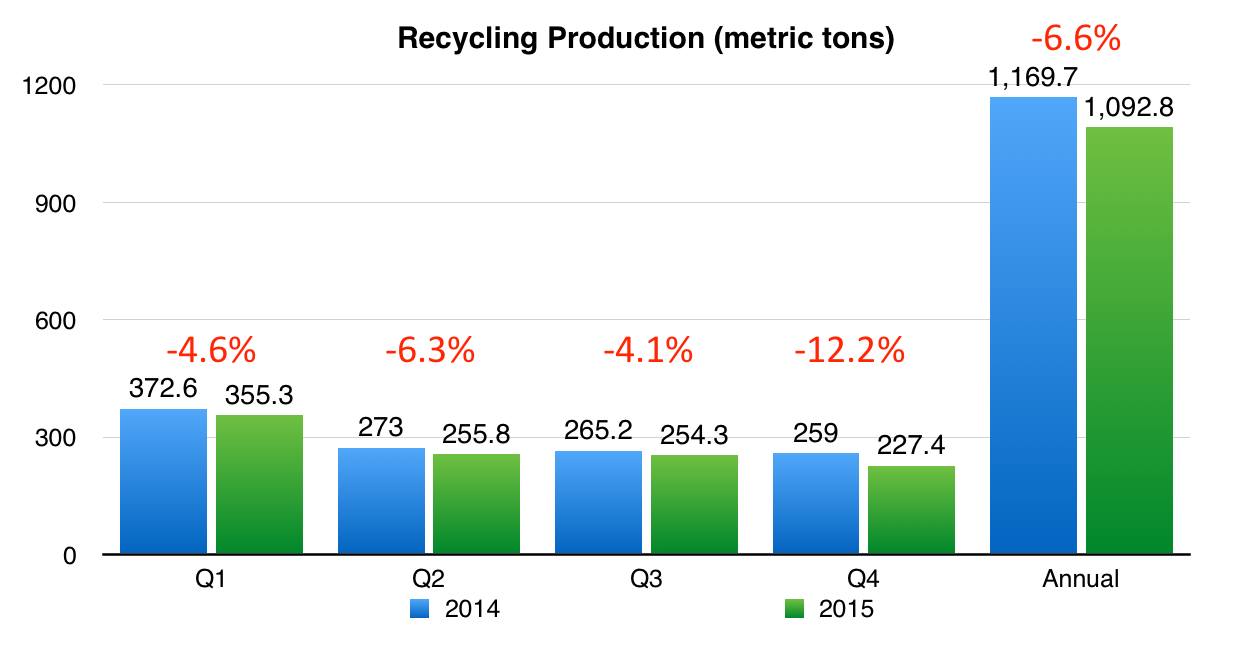

- Recycling levels have fallen precipitously.

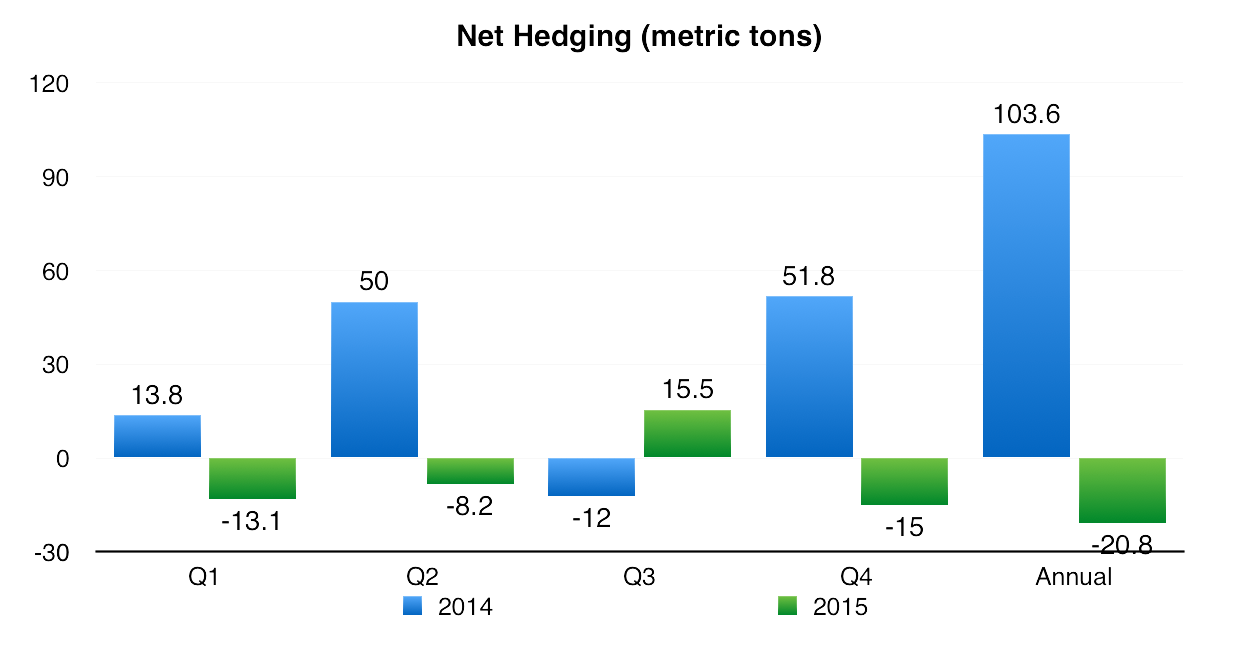

- Reversal in hedging activity indicates miners may believe prices have bottomed and will rally.

On Thursday, February 11, gold jumped over $50 per ounce, returning the metal to the headlines after years of decline. The timeless treasure began the millennium as low as $348.26 in April 2001 and rose to $1,905.30 in August 2011. The ten-year bull market then succumbed to a multi-year bear market that may be ending.

For investors, gold can seem like voodoo magic. Gold is said to hedge inflation, deflation, and overall risk. In 2011, when investors were snapping up gold in preparation for inflation, George Soros announced he had sold his gold holdings as he no longer feared deflation. How can investors properly value gold when its financial purpose is as fickle as investor sentiment?

This report attempts to move past the abstract “risk on” and “risk off” indicator and instead analyzes gold as one would any other commodity, by examining fundamental supply and demand. Many may point to global recession fears as the reason for gold’s spike on February 11, but this was also the day the World Gold Council released its “Gold Demand Trends Full Year 2015” report that indicates demand continues to exceed supply.