Background

Understanding the obstacle to higher equity valuesTaiwan’s economy is a strong foundation for equities

Taiwan is an island with 23 million people and the fifth largest economy in Asia. In 2014, Taiwan was the 19th largest economy in the world by PPP-adjusted GDP and 18th in PPP-adjusted GDP per capita according to the World Bank. Its nominal GDP (2014) was $505.45 billion (26th), which is export heavy at $318 billion. The island has an advanced economy composed 69% in services, 29% in industry, and 2% in agriculture. Major exports are electronics (computers, televisions, telecommunications), ships, petrochemicals, machinery, and textiles.

Currently, Taiwan’s technology-focused economy is relatively healthy compared to other emerging market economies, which rely on commodity exports to a slowing Chinese economy. Real GDP growth was 3.7% in 2014 and is forecast to be 1.4% and 2.4% in 2015 and 2016 respectively. Unemployment is low: reported at 3.8% in September for a labor force estimated at 11.6 million people. Inflation is low: CPI was 1.2% in 2014 and forecast to be -0.4% in 2015 and 1.2% in 2016. Taiwan recently reported a $14.7 billion current account surplus and has the fifth largest foreign reserves in the world at $425 billion. The sovereign credit ratings are AA- by S&P, Aa3 by Moody’s, and A+ by Fitch.

Taiwan has an active publicly-traded equity market. The strength of the equity market can be approximated through the MSCI Taiwan Index, which has futures and options that trade on the Singapore Exchange and an ETF that is traded on NYSE. MSCI Taiwan is comprised of 96 companies with a heavy weight towards the computer, semiconductor, and electronics industries. Taiwan Semiconductor (TSMC) makes up nearly 25% of the index.

Despite a strong foundation, Taiwanese equities have underperformedMSCI Taiwan has severely underperformed the S&P 500 and Shanghai Composite over the last 5 years. The below 5-year chart is adjusted to US dollars: S&P 500 (blue line) returned 66.1%, Shanghai Composite (green line) returned 33.5%, and MSCI Taiwan lost 12.3%.

Exhibit 1: 5-year MSCI Taiwan, S&P 500, Shanghai Composite Index Values

Internally, the Taiwanese equities market appears weak. Only 20 of the 96 companies in MSCI Taiwan are trading in the top 50% of their 52-week trading range. Only 5 of these companies belong to Taiwan’s core industry of technology (Core Industry Risk). Stocks that are performing well are in apparel, chemicals, financial services, packaged foods, and real estate industries. The bottom performing stocks in the index include 3 maritime shipping companies (Macro Risk), cement manufacturers (Macro Risk), a number of PC and LCD monitor manufacturers (Core Industry Risk), and surprisingly, Taiwan’s two airlines (Macro Risk), which should be benefiting from low jet fuel prices, but are likely pricing in fears of decreased Chinese tourism due to a slowing Chinese economy.

Taiwanese corporate earnings have been relatively strong, PE multiple is the problemActual earnings data shows that Taiwanese businesses are not underperforming American and Chinese corporations as much as Exhibit 1 indicates. Exhibit 2 illustrates MSCI Taiwan (white line), S&P 500 (blue line), and Shanghai Composite (green line) earnings over the past five years. The histograms below the line chart show the rate of change in corporate earnings.

Exhibit 2: 5-year MSCI Taiwan, S&P 500, Shanghai Composite Earnings

Exhibit 3 illustrates that MSCI Taiwan is actually underperforming due to a contracting PE multiple. The index traded at a 24 PE multiple in 2012 but the multiple has contracted to a mere 12.2 today. Historically, MSCI Taiwan has traded at an average multiple of 17.7. Regaining even a 16 PE ratio would result in MSCI Taiwan increasing from today’s 309 to 405, a 31% upside.

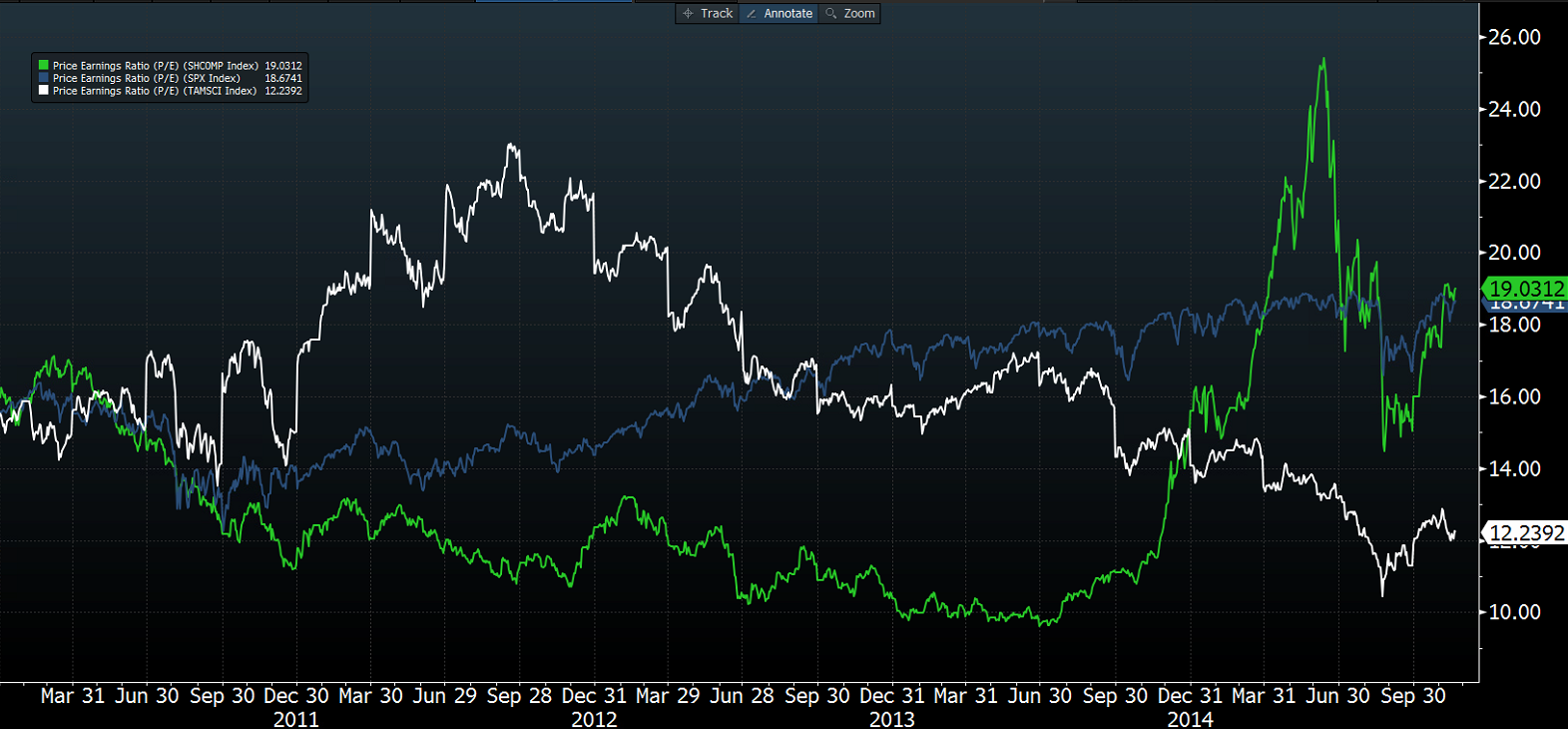

Exhibit 3: 5-year MSCI Taiwan, S&P 500, Shanghai Composite PE Multiples

MSCI Taiwan is cheaper than equity indices of many other countries, such as the S&P 500 at 18.1 and the Shanghai Composite at 19.0. Over the past five years, the S&P 500 has enjoyed consistent multiple expansion and the Shanghai Composite recently had a multiple spike in mid-2015 as stock trading became popular in China. Why is the PE multiple of MSCI Taiwan contracting? Why are investors not willing to pay as much for a dollar of earnings in Taiwan than they are in other countries?